🍼 Why Maternity Cover in Health Insurance Matters — And Why It’s Often Missing When You Need It Most

Childbirth is a joyful moment. But for many Indian families, it also becomes a moment of financial stress — especially when the hospital bill comes as a surprise. Despite rising maternity healthcare costs, most individual health insurance policies either exclude or limit maternity coverage.

Strangely, group health insurance (usually offered by employers) provides better protection — raising the question: Why does maternity insurance remain so underused and misunderstood in India?

Let’s decode the gap, the risks, and what smart policyholders should know before it’s toolate.

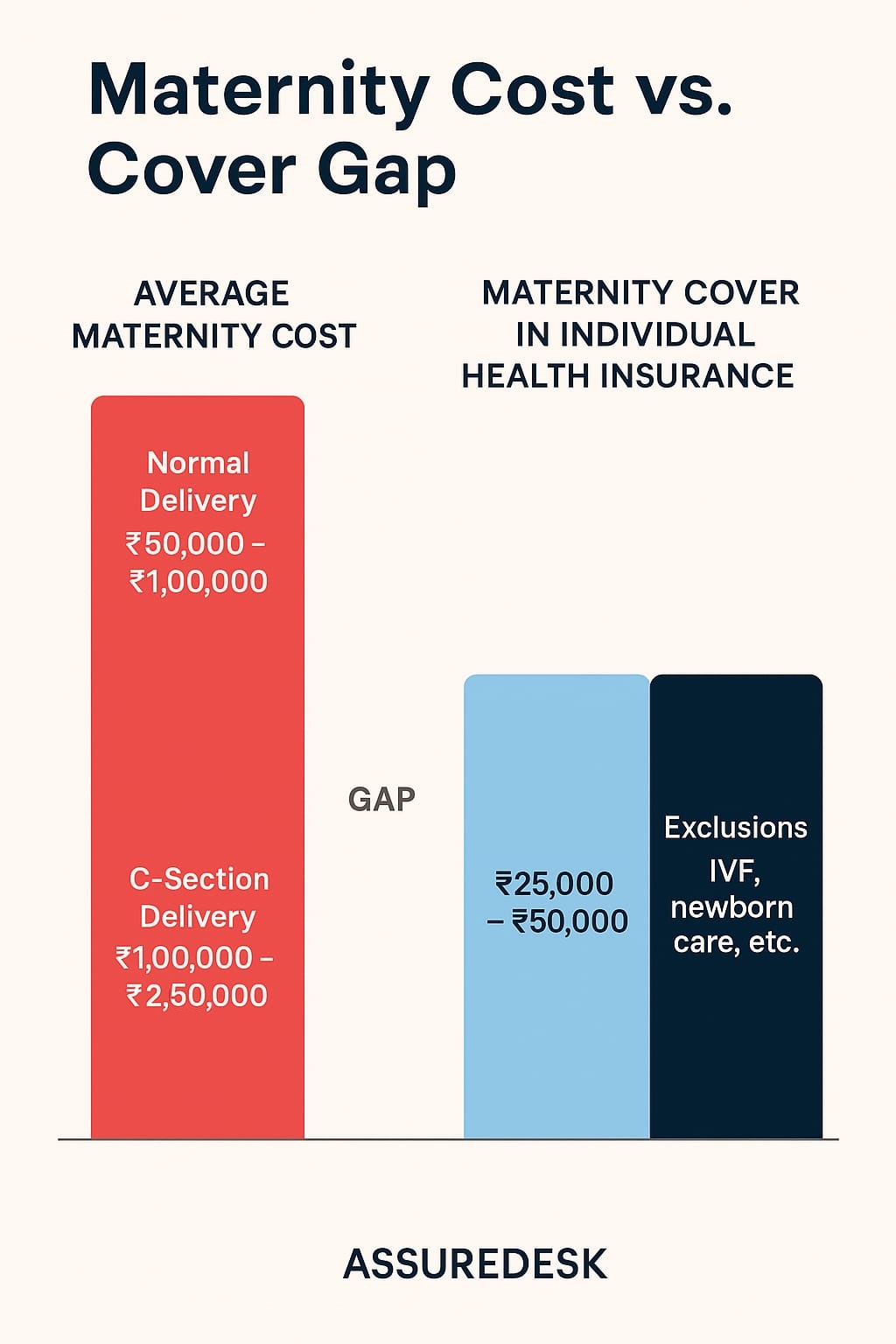

💸 The Rising Cost of Maternity in India

Here’s what urban families are paying on average:

| Type of Expense | Estimated Cost (INR) |

|---|---|

| Normal delivery | ₹50,000 – ₹1,00,000 |

| C-section delivery | ₹1,00,000 – ₹2,50,000 |

| NICU (Neonatal Intensive Care Unit) /per day | ₹5,000 – ₹15,000 |

| Pre-natal tests & scans | ₹10,000 – ₹30,000 |

| Post-natal care & meds | ₹5,000 – ₹15,000 |

These are baseline estimates — in metros like Mumbai, Delhi, or Bangalore, the cost can go much higher in premium hospitals.

🛑 Why Most Maternity Claims Get Rejected

Even when a policy claims to offer maternity coverage, the fine print often hides roadblocks:

-

Long Waiting Periods

-

Usually 2 to 4 years before claims are allowed.

-

-

Low Sub-limits

-

Cover capped at ₹25,000–₹50,000 — barely 20–30% of actual cost.

-

-

Exclusions

-

IVF, infertility treatments, congenital defects, or twins often excluded.

-

-

Newborn Cover Issues

-

Newborns may not be covered for NICU or emergency care unless added immediately.

-

-

One-time Limitations

- Some plans cover only the first delivery or a fixed number of pregnancies.

🏢 Group Health Insurance Covers What Individual Plans Don’t

If you're working in a mid-to-large company, chances are your employer’s group health policy offers maternity benefits:

| Feature | Group Health Plan | Individual Health Plan |

|---|

| Waiting period | 0–9 months (or none) | 2–4 years |

| Maternity cover limit | ₹75,000 – ₹1.5 lakh | ₹25,000 – ₹50,000 |

| Newborn cover | Often included | Rarely included |

| IVF/complication cover | Sometimes included | Mostly excluded |

The downside? Coverage ends when you resign, retire, or switch jobs. You can’t rely on group health forever.

🤔 Why Isn’t Maternity Cover Popular in Individual Health Plans?

Insurers see it as "high risk, low benefit" from their side:

-

Maternity is a planned event — people buy insurance only to claim it quickly.

-

It creates adverse selection (claim-first-buy-later behavior).

-

Long waiting periods discourage young couples.

-

Insurers don’t actively market maternity riders due to these challenges.

✅ What to Look for in a Good Maternity Cover

If you're newly married or planning to start a family, be proactive. Look for:

-

✔️ Shorter waiting periods

-

✔️ Coverage for C-section and NICU

-

✔️ Post-natal expenses included

-

✔️ Newborn baby coverage (at least 90 days)

-

✔️ Option to convert from group to individual post-employment

📊 The Data Reality: India’s Maternity Coverage Gaps

-

Only ~20% of individual health policies offer maternity benefits.

-

Up to 40% of maternity claims are either rejected or partially paid due to sub-limits and exclusions.

- In contrast, 70%+ of group insurance policies in Tier 1 companies cover maternity expenses fully or substantially.

🔍 How Assuredesk Can Help

Not all policies are maternity-friendly — and many agents won't warn you until it's too late. Assuredesk helps you:

-

-

✅ Compare maternity benefits across insurers

-

✅ Understand exclusions & waiting periods

-

✅ Get advice tailored to your life stage

- ✅ Decode your current policy’s fine print — free of cost

-

💬 Final Word

Maternity isn’t a medical emergency — but financially, it can become one without proper cover.

Whether you're single, newly married, or planning a baby in the next 2–3 years, your best time to act is today.

Choose a plan that supports your family’s journey — from pregnancy to delivery to newborn care.

🍼 हेल्थ इंश्योरेंस में मैटरनिटी कवर क्यों ज़रूरी है – और ये ज़रूरत के वक़्त क्यों अक्सर गायब होता है

बच्चे का जन्म एक खुशी का पल होता है, लेकिन कई भारतीय परिवारों के लिए यह आर्थिक बोझ बन जाता है — खासकर जब अस्पताल का बिल हाथ में आता है।

आज जब डिलीवरी का खर्च लगातार बढ़ रहा है, तब भी ज्यादातर व्यक्तिगत (individual) हेल्थ इंश्योरेंस पॉलिसी मैटरनिटी को या तो कवर ही नहीं करती या फिर बहुत सीमित रूप से करती हैं।

वहीं दूसरी ओर, ग्रुप हेल्थ इंश्योरेंस (जो कंपनियों द्वारा कर्मचारियों को दी जाती है) बेहतर मैटरनिटी कवर देती है। सवाल उठता है — आख़िर क्यों व्यक्तिगत योजनाओं में यह सुविधा नहीं होती जब सबसे ज़्यादा ज़रूरत होती है?

💸 भारत में मैटरनिटी का बढ़ता खर्च

आज के समय में एक बच्चे के जन्म का औसत खर्च:

| खर्च का प्रकार | अनुमानित राशि (₹ में) |

|---|---|

| सामान्य डिलीवरी | ₹50,000 – ₹1,00,000 |

| सी-सेक्शन डिलीवरी | ₹1,00,000 – ₹2,50,000 |

| एनआईसीयू (प्रति दिन) | ₹5,000 – ₹15,000 |

| प्री-नेटल टेस्ट व स्कैन | ₹10,000 – ₹30,000 |

| डिलीवरी के बाद की दवा व देखभाल | ₹5,000 – ₹15,000 |

मेट्रो शहरों में यह खर्च और भी ज्यादा हो सकता है, खासकर प्राइवेट अस्पतालों में।

🛑 मैटरनिटी क्लेम रिजेक्ट क्यों होते हैं?

पॉलिसी में मैटरनिटी कवर होने के बावजूद कई अड़चनें होती हैं:

-

लंबा वेटिंग पीरियड

-

आमतौर पर 2 से 4 साल।

-

-

कम सब-लिमिट

-

₹25,000–₹50,000 तक की सीमा — जो असल खर्च का केवल 20–30% होती है।

-

-

महत्वपूर्ण बातों का एक्सक्लूज़न

-

IVF, जुड़वा बच्चों की डिलीवरी, नवजात बीमारियाँ अक्सर कवर नहीं होतीं।

-

-

नवजात शिशु का कवर नहीं

-

तुरंत शामिल न करने पर बच्चों के इलाज का खर्च बाहर हो सकता है।

-

-

केवल पहली डिलीवरी का कवर

- कई पॉलिसी केवल एक बार की डिलीवरी को ही कवर करती हैं।

🏢 ग्रुप हेल्थ इंश्योरेंस में बेहतर मैटरनिटी कवर क्यों होता है

अगर आप किसी कंपनी में काम कर रहे हैं, तो आपकी कॉर्पोरेट ग्रुप हेल्थ पॉलिसी में बेहतर मैटरनिटी बेनिफिट्स हो सकते हैं:

| फीचर | ग्रुप पॉलिसी | व्यक्तिगत पॉलिसी |

|---|---|---|

| वेटिंग पीरियड | 0–9 महीने (या नहीं) | 2–4 साल |

| मैटरनिटी कवर लिमिट | ₹75,000 – ₹1.5 लाख | ₹25,000 – ₹50,000 |

| नवजात शिशु का कवर | अक्सर शामिल | बहुत कम मामलों में |

| IVF / जटिलताओं का कवर | कभी-कभी | लगभग हमेशा एक्सक्लूडेड |

लेकिन ध्यान दें: नौकरी बदलते ही यह कवर खत्म हो जाता है। इसे परमानेंट नहीं माना जा सकता।

🤔 व्यक्तिगत पॉलिसियों में मैटरनिटी कवर क्यों नहीं लोकप्रिय है?

बीमा कंपनियाँ इसे "अधिक जोखिम वाला, कम लाभकारी" मानती हैं:

-

मैटरनिटी एक प्लान किया हुआ खर्च होता है – लोग सिर्फ क्लेम करने के लिए पॉलिसी लेते हैं।

-

इससे मोरल हैज़र्ड (claim-first, exit-later) बढ़ता है।

-

लंबा वेटिंग पीरियड ग्राहकों को निराश करता है।

- कंपनियाँ इसे एक्टिव रूप से प्रमोट नहीं करतीं।

✅ अगर आप फैमिली प्लान कर रहे हैं, तो इन बातों का ध्यान रखें

अभी से तैयारी करें — डिलीवरी के पहले ही पॉलिसी लें जिसमें मैटरनिटी शामिल हो:

-

-

✔️ छोटा वेटिंग पीरियड

-

✔️ C-सेक्शन व NICU का खर्च कवर

-

✔️ नवजात शिशु का कवर (कम से कम 90 दिन)

-

✔️ प्री और पोस्ट-नेटल खर्च भी शामिल

- ✔️ ग्रुप से व्यक्तिगत में कन्वर्ज़न का विकल्प

-

📊 आंकड़े क्या कहते हैं:

-

-

-

भारत में केवल ~20% व्यक्तिगत हेल्थ पॉलिसी मैटरनिटी कवर देती हैं।

-

करीब 40% मैटरनिटी क्लेम रिजेक्ट या आंशिक रूप से मंज़ूर होते हैं।

- वहीं, 70% से अधिक ग्रुप पॉलिसी पूरा या पर्याप्त कवर देती हैं।

-

-

🔍 Assuredesk कैसे मदद करता है?

हर पॉलिसी में मैटरनिटी फ्रेंडली फीचर्स नहीं होते — और एजेंट आपको पूरी जानकारी नहीं देते। Assuredesk पर आप:

-

-

-

-

✅ विभिन्न बीमा कंपनियों की तुलना कर सकते हैं

-

✅ वेटिंग पीरियड और एक्सक्लूज़न समझ सकते हैं

-

✅ आपके लाइफस्टेज के अनुसार सलाह पा सकते हैं

-

✅ मौजूदा पॉलिसी का विश्लेषण (फ्री में) करवा सकते हैं

-

-

-

💬 निष्कर्ष:

मैटरनिटी कोई इमरजेंसी नहीं है — लेकिन अगर बीमा कवर न हो, तो यह आर्थिक इमरजेंसी बन सकती है।

अगर आप सिंगल हैं, नवविवाहित हैं या कुछ वर्षों में फैमिली प्लान कर रहे हैं, तो अभी सही पॉलिसी चुनना बेहद ज़रूरी है।